Financing operations — from working capital to investment projects on tailored terms

Financing of investments, modernization, and business expansion

Financing to cover cash gaps and support business turnover growth

Construction financing using escrow accounts

Support for exports and development of international business

Financing of energy-efficient and environmental projects with support from international financial institutions

Procurement of vehicles for official and operational needs

Fast financing for business

Solutions for women entrepreneurs to grow their business

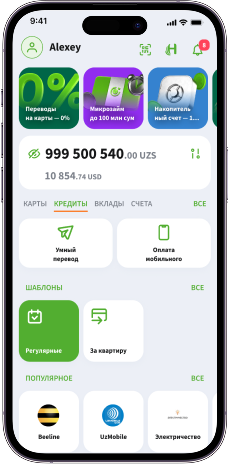

Get access to all the benefits of the payroll project and other Ipoteka Bank services in just a few seconds.